If you've ever wondered whether putting all your insurance with one company actually saves money, you're asking the right question. The honest answer is it depends. Bundling can meaningfully reduce your total premium, but only if the insurer base rates are competitive and the coverage you're comparing is actually equivalent. Here's what Ontario homeowners need to know before making that call.

Morison Insurance is an Ontario brokerage, not a single carrier. That means we compare bundled options across dozens of insurers to find what actually works for your household, rather than defaulting to one company because it's convenient.

What "Bundling With One Company" Really Means

Bundling simply means placing more than one insurance policy with the same insurer and receiving a multi-policy discount in return. The most common version is bundled home & auto insurance, but the concept extends further: condo or tenant insurance paired with auto, and additions like recreational vehicles (ATVs, boats, RVs, snowmobiles) or cottage insurance are all common bundle expansions. For households that want a higher level of liability protection, adding umbrella coverage to a home and auto bundle is often the most meaningful upgrade available.

One important clarification worth making early: working with a broker like Morison doesn't mean you lose the simplicity of dealing with one company. You can absolutely end up with a single insurer, but you'll arrive there after the math has been done, not before. The "one company" decision should follow the comparison, not replace it.

How Bundle Discounts Work (and Why Bundling Can Be Cheaper Without Cutting Coverage)

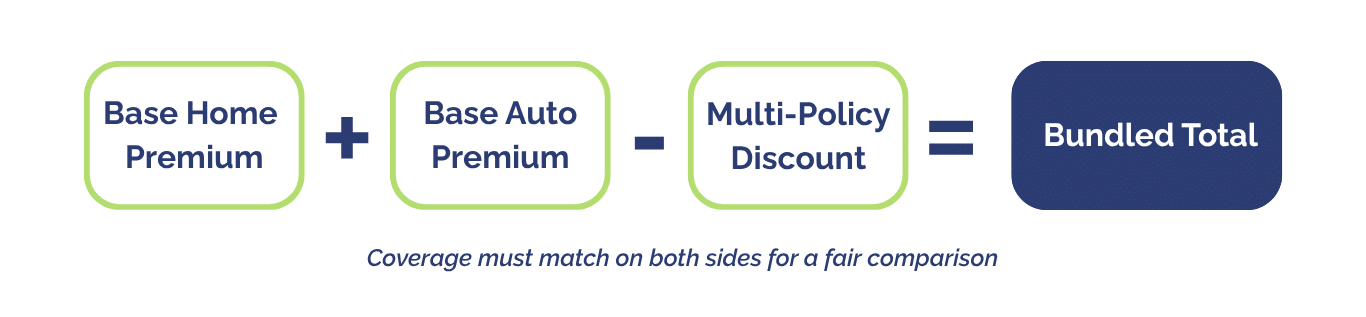

The mechanics are straightforward. Each policy — home insurance, auto insurance, condo insurance — carries its own base premium, calculated from your specific risk profile. When you place a second (or third) policy with the same insurer, they apply a multi-policy discount to one or both policies. Your final cost is those base premiums minus the discount.

Multi-policy discounts at Morison typically range from 5% to 25% depending on the insurer and your profile. But that range is only meaningful if the base premiums are competitive. A 20% discount on an overpriced base rate may still leave you paying more than you would with a split approach using two well-priced carriers, which is exactly why comparing both options matters.

One point worth addressing directly: a lower bundled quote doesn't automatically mean you're better protected. Cheaper quotes sometimes reflect reduced liability limits, higher deductibles, or different replacement cost assumptions rather than genuinely better pricing. Ontario's Financial Services Regulatory Authority (FSRA) has specifically flagged that undervaluing your home or contents can leave you without sufficient coverage when a claim arises. A bundle should lower your cost, not your protection.

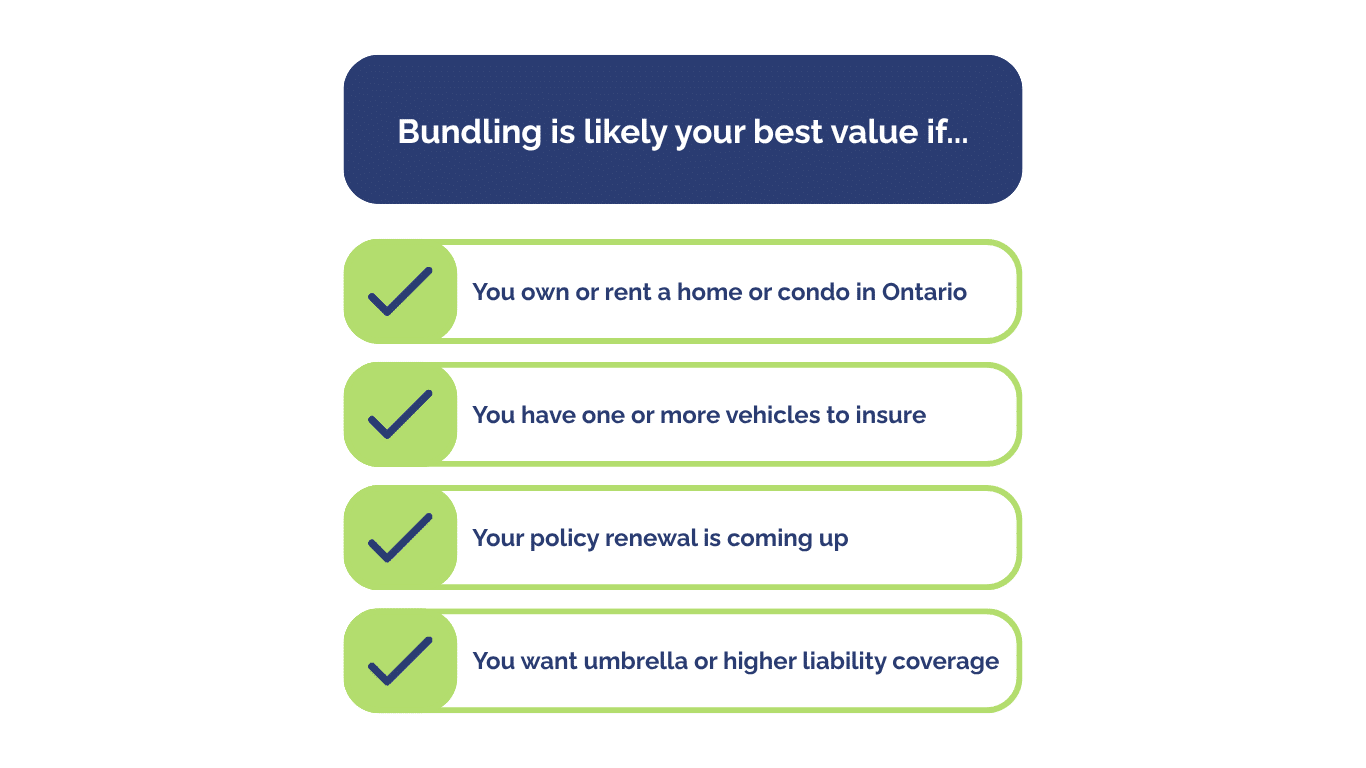

When Bundling With One Insurer Is Usually the Best Deal

Bundling tends to win when your policies fit standard underwriting criteria well: a homeowner with one or two vehicles, a reasonably clean claims history, and renewal dates that can be aligned. In these cases, the discount applies to a meaningful combined premium, and the savings are real.

The value compounds further when you add umbrella liability coverage. A home, auto, and umbrella bundle is the configuration that is often recommended for established Ontario households because it extends your liability protection well beyond standard policy limits. It would cover large claims, legal defence costs, and situations where a single incident could create serious financial exposure. There's also a structural reason bundling makes sense here: most insurers require umbrella coverage to sit with the same company as your underlying home and auto policies. That requirement makes bundling a practical necessity for households that want comprehensive protection, not just a pricing consideration.

One other frequently cited perk is the single deductible. Some bundled policies require only one deductible if your home and vehicle are both damaged in the same incident. That said, this varies by insurer and policy structure. Your Morison broker will clarify how your specific bundle handles deductibles.

When Splitting Policies Can Be Cheaper (Even After the Bundle Discount)

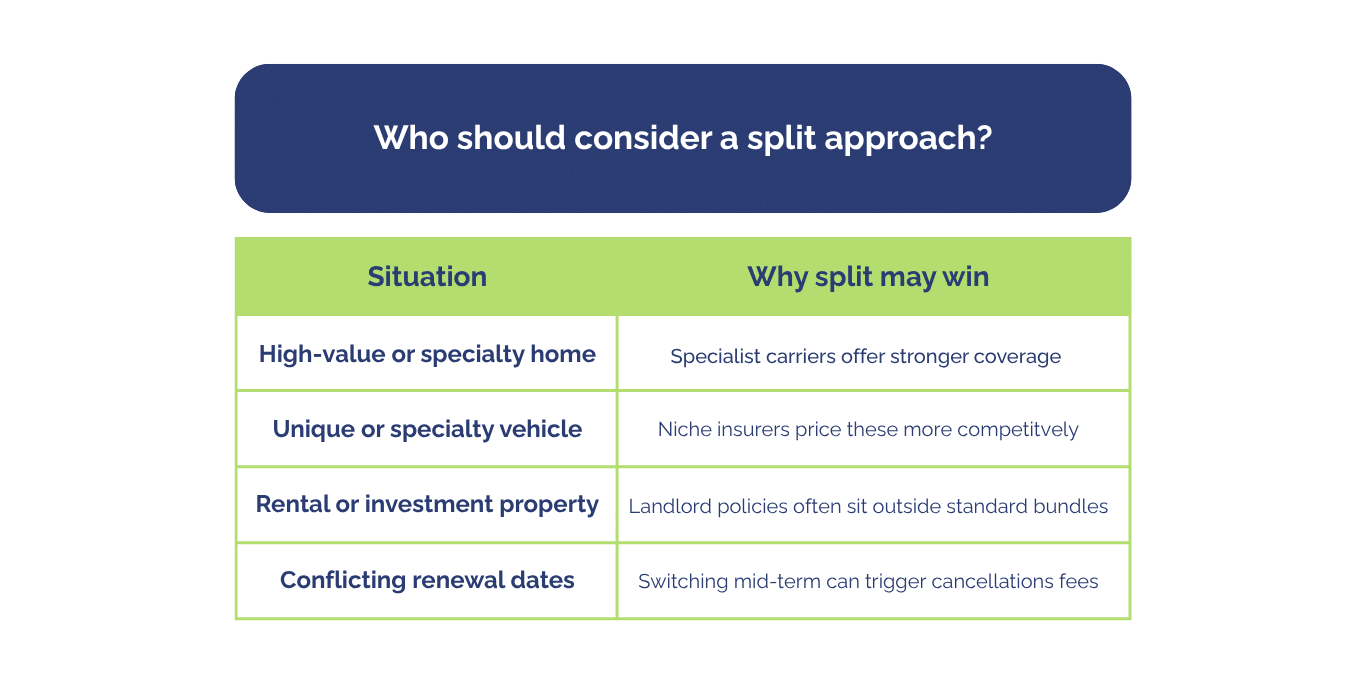

The discount becomes irrelevant if one insurer's base rate for a particular line is simply uncompetitive. A carrier that offers an excellent auto rate but prices home insurance aggressively may still cost more in a bundle than two well-matched carriers operating separately, even after the multi-policy discount is applied.

This matters particularly for non-standard situations. Unique or high-value homes, specialty vehicles, rental properties, and certain recreational property configurations often require specialist carriers whose strength is in that one line. Bundling everything with a generalist insurer in those cases can produce a coverage gap, an uncompetitive premium, or both.

Conflicting renewal dates can also complicate bundling in the short term, although this is a timing issue a broker can help you navigate, not a reason to avoid bundling permanently.

How to Compare Bundle vs Split Quotes the Right Way in Ontario

The single most important rule is apples-to-apples: the only fair comparison is one where both quotes reflect the same liability limits, deductibles, replacement cost methodology, and endorsements. If a bundled quote is cheaper because it carries a lower liability limit, that's not savings; that's a coverage reduction dressed up as a discount.

From a compliance standpoint, Ontario's FSRA requires that consumers provide accurate, complete information and promptly notify their insurer if circumstances change in ways that could affect their coverage. This matters practically when households change: a teenager earning their licence, a new driver moving in, or a significant renovation all affect your risk profile and need to be disclosed. Morison's brokers specifically note the obligation to advise of all licensed drivers residing in your household. Getting this right protects you at claim time.

It's also worth understanding the difference between lowering cost through bundling and lowering cost by giving something up. Since January 2024, Ontario drivers can elect not to claim under Direct Compensation for Property Damage (DCPD) in certain situations, but the regulator advises speaking with a broker before making that decision, because opting out means literally giving up coverage. That's a different thing from bundling. The goal of a bundle is to lower cost while keeping protection intact; that distinction is worth keeping front of mind when reviewing any quote.

Why Using a Broker Changes the Answer (Even If You Want "One Company")

Here's the practical upside of working with an independent broker: you can still end up with one insurer and one bundled policy, but you'll know it's genuinely competitive because alternatives were tested. That confidence is something you simply can't get by going directly to a single carrier.

Morison's brokers compare bundled options across 50+ Canadian insurers, which means the "best bundle" isn't determined by which carrier happens to have the most recognizable name. It's determined by which carrier offers the best combination of base pricing, discount, coverage terms, and claims service for your specific profile. That comparison is what we've been doing for Ontario households since 1923.

If you're mid-term on existing policies, there may be cancellation fees to factor in. Your broker will calculate whether switching immediately or waiting until renewal produces better overall value; it's not always worth moving right away, but it's always worth knowing the numbers.

Find Out If Bundling Is Actually Cheaper for You (Without Cutting Coverage)

Bundling can be one of the most effective ways to reduce your total insurance cost — but the savings are only meaningful if the coverage underneath is sound and the base pricing is competitive. The smartest move is to compare a bundled quote and a split-policy quote side by side, with equivalent coverage on both sides of the ledger.

Morison's brokers do exactly that across dozens of Canadian insurers. If a bundle wins, you'll know why. If a split approach comes out ahead, you'll know that too. And if your household is a good fit for umbrella coverage, we can walk you through home, auto, and umbrella protection as a package.

Ready to find out how much you could save?