What Is a Home and Auto Insurance Broker?

A home and auto insurance broker is an independent professional who works with multiple insurance companies, not just one. In Ontario, brokers are licensed and regulated by the Registered Insurance Brokers of Ontario (RIBO), meaning they've met education and ethical standards before advising you on coverage.

Unlike agents who represent a single insurer, brokers work on your behalf. They shop around, compare home and auto policies (including bundling options), and present choices rather than pushing one company's products. They review unique risks such as:

- Property location

- Vehicle usage

- Driving record

- Liability needs

They recommend coverage you might not realize you need — sewer backup, enhanced accident benefits — and help ensure you aren't underinsured or missing key protections.

One often-overlooked benefit: Morison Insurance brokers assist you through the claims process, acting as your advocate when something goes wrong. They explain what's covered, outline next steps, and communicate with the insurer on your behalf if issues arise.

Step 1: Understand Your Home and Auto Insurance Needs

Before getting quotes, have a clear picture of what you need to protect. Knowing your needs helps your broker recommend the right policy — not just the cheapest one.

Don't Overlook Personal Liability

Personal liability coverage on both policies protects you if someone is injured on your property or you accidentally cause harm to others.

What to Know Before You Quote

Home insurance

- Your dwelling's rebuild cost

- The value of your belongings

- Common exclusions — many standard policies don't cover sewer backup or overland water flooding; additional endorsements may be needed

Auto insurance

- Liability limits — many experts recommend exceeding the legal minimum

- Collision and comprehensive coverage

- A deductible you can comfortably afford

Step 2: How Home and Auto Insurance Brokers Get and Compare Quotes

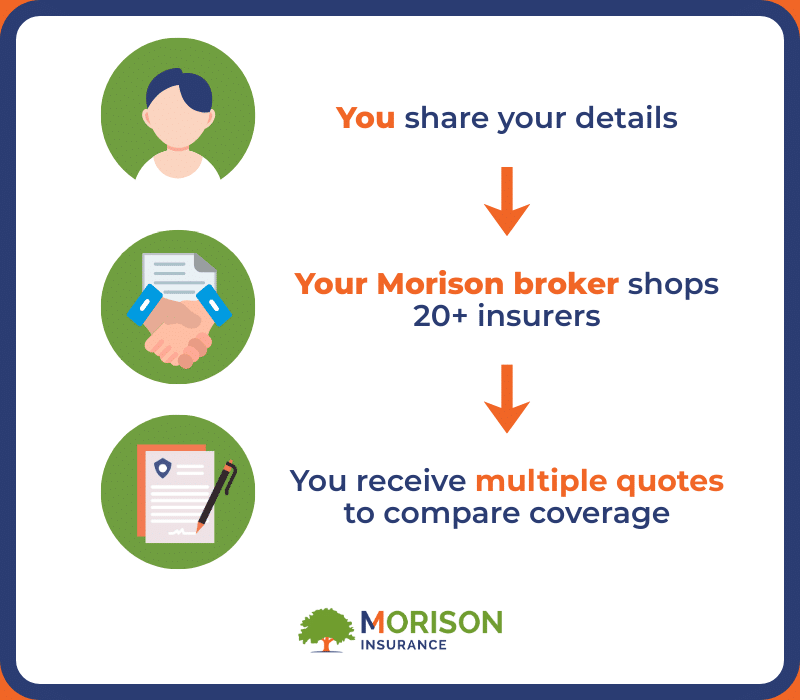

Once you've identified your coverage needs, a broker takes over the legwork. They collect your details once — home information (age, square footage, updates) and vehicle details (make, model, driving record) — then shop multiple insurers on your behalf, comparing quotes on an apples-to-apples basis. Finally, they present your options, explaining pros and cons in plain language, including whether bundling makes sense for your situation.

Get Quotes Yourself | Use a Broker | |

Time spent | Hours researching companies, filling out multiple forms, and comparing quotes on your own | One conversation: your broker handles the shopping and comparison for you |

Number of insurers compared | Limited to companies you know about or find online | Access to dozens of insurers, including some not available direct-to-consumer |

Level of expertise | You rely on your own knowledge of coverage options and industry terms | Licensed professionals who understand policy details, exclusions, and endorsements |

Risk of missing discounts | High: you may not know which discounts exist or how to qualify | Low: brokers know available discounts and ensure you receive everything you're eligible for |

Help understanding policy details | You interpret policy documents on your own | Your broker explains coverage, exclusions, and fine print in plain language |

Support during claims | You deal directly with the insurance company | Your broker advocates on your behalf and helps navigate the claims process |

Want help finding the right coverage? Get a quote from Morison Insurance.

Step 3: How to Evaluate a Home and Auto Insurance Broker

Not all brokers are the same. Here's what to look for:

- Licensing and credentials: Ensure your broker is RIBO licensed in Ontario. Additional designations like CIP or CAIB indicate advanced training.

- Experience with home and auto: You want someone comfortable handling both types of coverage and bundling policies.

- Number of insurers: More insurance partners means more options and better chances of finding competitive pricing.

- Reviews and reputation: Look at Google reviews, industry awards, and explore feedback from clients.

- Responsiveness: How quickly do they respond? Slow replies during quoting often mean slow support during claims.

- Claims support: Ask if they help clients through claims. A broker who advocates for you during difficult situations is invaluable."

Step 4: How to Choose the Right Home and Auto Insurance Policy with Your Broker

Once your broker presents options, make sure you're comparing like-for-like coverage. Confirm key limits such as home rebuild cost, liability amounts, and vehicle coverage. Ask your broker to explain what's covered, what's excluded, and which optional endorsements might be worth adding.

The Cheapest Quote Isn't Always the Best Value

A policy with major coverage gaps could cost far more if something goes wrong. When choosing the right insurance policy, value matters more than headline price.

What Working With a Broker Really Costs — and What You Save

Two of the most common questions Ontario homeowners ask before working with a broker:

Do Home and Auto Insurance Brokers Cost More?

- Brokers are typically paid by the insurance companies they work with — not through additional fees charged to you.

- You pay the same premium as you would going direct.

- You gain expert advice, multi-insurer shopping, and ongoing support throughout your policy term.

- You're already paying for insurance; you might as well get expert help with it.

Can Brokers Help Me Save on Home and Auto Insurance?

- Apply available discounts you qualify for: multi-policy, good driver, winter tire, home alarm, and more.

- Decide whether bundling your home and auto policies makes sense for your situation.

- Suggest deductible options to balance your premium against what you can afford out-of-pocket if you make a claim.

- Walk you through additional ways to save: usage-based programs, safety features, and home upgrades. See also car insurance discounts and home insurance discounts.

How Bundling Home and Auto Through a Broker Works

Bundling means combining your home and auto insurance policies with the same insurer.

Typical Benefits

- Fewer bills to manage

- Aligned renewal dates

- Potential savings often up to 25% or more off your premiums

A broker is well-positioned to evaluate whether bundling is actually the best choice for you. In some cases, keeping policies with separate carriers might offer better coverage or pricing for your specific situation. Your broker can compare both scenarios and recommend the approach that makes the most sense.

Talk to a Home and Auto Insurance Broker in Ontario

Ready to find the right home and auto coverage for your needs?

Speak with a friendly, RIBO-licensed Morison Insurance broker. We compare quotes from multiple insurers, explain your options in plain language, and help you bundle your home and auto insurance for the right balance of coverage and price.

Call 1-800-463-8074 or request a quote to get started.