More Ontario families than ever own not just one home, but two. Perhaps you've purchased a condo in Toronto to avoid the daily commute from Burlington, or you're maintaining a second property in St. Catharines during renovations.

If you're in this position, you're probably wondering how a second home affects your insurance and taxes.

In this article, we're focusing on secondary homes. Properties you use regularly but don't live in full-time. This is different from seasonal cottages. We're talking about condos, apartments, and houses that serve as your second residence, not rental properties.

Understanding the difference between a primary residence and a secondary home affects your home insurance or condo insurance premiums, tax obligations, and mortgage terms. At Morison Insurance, our brokers help Ontario homeowners protect both properties through our network of more than 25 insurance carriers.

Your primary residence is the home where you live most of the year, the address on your driver's license and where you spend the majority of your time.

A secondary home is another property you own and use frequently, but not as your main dwelling. This could be an apartment you stay in during the workweek, a condo you use on weekends, or a property for family members.

This distinction matters for:

|

Feature |

Primary Residence |

Secondary Home |

|

Main Use |

Where you live most of the year |

Second property you use regularly |

|

Occupancy |

Continuous |

Part-time or shared |

|

Example |

Family home in Burlington |

Condo in Toronto for weekdays |

|

Coverage Needs |

Standard home policy |

Separate secondary home policy |

According to the Canada Revenue Agency (CRA), your primary residence is the home you "ordinarily inhabit." Your family unit can only designate one property as your principal residence per year.

This matters when you sell. If you've designated a home as your principal residence for all the years you owned it, you may be exempt from capital gains tax on any profit.

Example: Family home in Oakville (primary residence) and Toronto condo used on weekdays (secondary home). The CRA allows just one designation each year.

Not sure which home counts as your primary residence? Speak with a Morison Insurance broker for guidance. Ensuring your insurance classification matches your tax designation helps avoid confusion when filing a claim.

A secondary home is a property you own and use frequently, but it's not where you live most of the time. Common examples include:

What a secondary home is NOT:

Critical: Your primary home insurance policy does not cover your secondary home. Insurance doesn't transfer between properties.

If you rent out your secondary home occasionally, disclose this to your insurer. You may need short-term rental coverage or a landlord insurance policy.

If your second property is a cottage or used only seasonally, that falls under a different type of insurance: seasonal or cottage insurance.

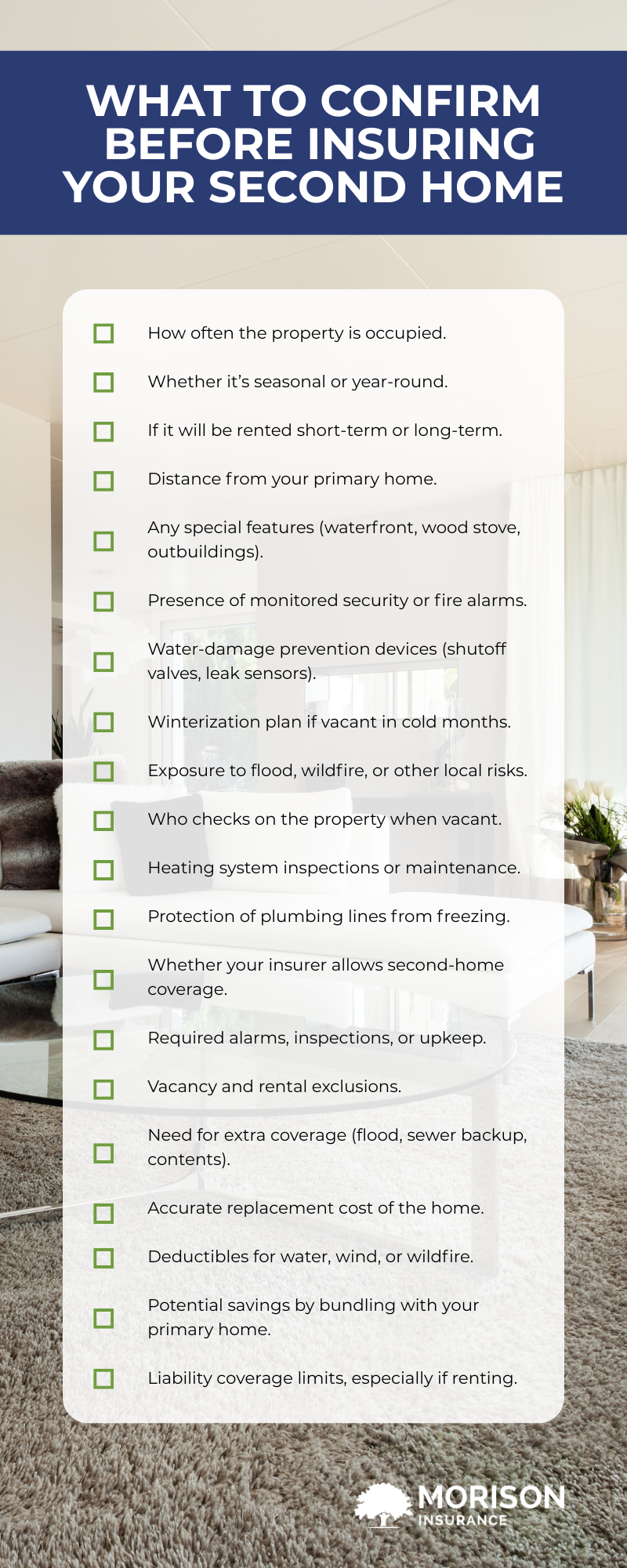

Understanding how insurance coverage works for primary vs secondary homes helps you make sure both properties are properly protected.

Both homes need separate policies. Your primary home policy won't automatically extend to your secondary home.

Primary residence insurance is designed for homes where you live full-time. Because you're there every day, you're more likely to notice problems early, which means lower risk for insurers.

Key features:

Secondary residence insurance accounts for periods when the property sits empty. Even weekend visits leave gaps in occupancy that create additional risks.

Key differences:

Second home buildings insurance addresses unique risks of part-time occupancy. Morison Insurance brokers ensure appropriate coverage through our network of 25+ carriers.

The type of insurance you need changes significantly if you rent out your second home, even for short periods. Standard homeowner's insurance does not cover rental activities.

If you don't inform your insurer about rental activity and file a claim, it may be denied because you didn't have the right coverage.

For more guidance: Rental Property Insurance: The Right Way | First-Time Landlord Guide

Your primary residence may qualify for the principal residence exemption—no capital gains tax on increases in value during designated years.

Your secondary home is usually subject to capital gains tax unless strategically designated as your principal residence for certain years.

Key points:

Keep insurance classification aligned with tax designation.

This article does not constitute tax advice. Consult an accountant about your situation.

When you're financing a second home, lenders look at things differently than they do for your primary residence. Here's what to expect:

Primary Residence:

Secondary Home:

Be transparent about property use. Misrepresenting plans can violate mortgage terms.

Tax Rules:

Insurance Requirements:

Mortgage Requirements:

The Urban Commuter: Burlington home, Toronto condo for workweeks. Both need separate policies.

Multi-Generational Property: Home near Hamilton campus for children attending university requires second home buildings insurance.

Renovation Project: Living elsewhere during construction. Both properties need appropriate coverage.

Flexible Worker: Homes in both St. Catharines and Toronto. One primary, one secondary. Both need separate policies.

Contact a Morison Insurance broker to discuss your secondary home insurance needs.

Owning two properties comes with added responsibility. These steps help ensure both your primary and secondary homes are properly protected:

Make sure each home is insured based on how you actually use it. Your primary residence needs a standard homeowner's policy, while your secondary home needs a policy that accounts for periods of vacancy.

Morison Insurance works with 25+ carriers for competitive multi-property rates. Bundling your primary home, secondary home, and auto insurance can lead to significant savings.

Bundled home and auto insurance →

Water leak detectors, smart thermostats, security cameras, and smart locks. Many insurers offer discounts.

Update your broker if usage changes. Visit your secondary home every two weeks to avoid vacancy issues.

No. You can only designate one property as your primary residence per family per year for tax purposes.

Yes. Each property must have its own policy. Homeowners insurance on second home properties doesn't extend from your primary residence.

Yes, if you live in your main home most of the time and use the condo part-time. Example: Burlington home with Toronto condo for workweeks.

Not usually, unless you designate it as your primary residence for certain years. Requires careful tax planning with an accountant.

Yes, but disclose this to your insurer. You'll need rental endorsements or landlord coverage. Standard policies don't cover rental activities.

Owning two homes enhances your lifestyle, but only if both are insured correctly.

Primary residence = home where you live most of the year and designate for tax purposes.

Secondary home = frequently used additional residence (not seasonal cottage) you own but don't occupy full-time.

Each has unique insurance requirements, tax implications, and lending considerations. Misclassifying properties or assuming coverage transfers can leave you financially exposed.

At Morison Insurance, we understand the complexities Ontario homeowners face. Our brokers work with more than 25 insurers to find the right protection for both properties. With 4,500+ five-star reviews, we provide clear, honest guidance.

Whether purchasing a secondary property in Toronto, Hamilton, Burlington, or St. Catharines, we'll help you understand what coverage you need.

Ready to properly insure your primary and secondary homes?

Get a quote from Morison Insurance →

Our team will review your situation, explain options across our carrier network, and build a coverage plan that protects what matters most.

This content is written by our Morison Insurance team. All

information posted is merely for educational and informational purposes. It is

not intended as a substitute for professional advice. Should you decide to act

upon any information in this article, you do so at your own risk. While the

information on this website has been verified to the best of our abilities, we

cannot guarantee that there are no mistakes or errors.