If you're shopping for home and auto insurance in Ontario, you've probably wondered whether working with a broker is worth it, or if you should just go directly to an insurer. It's a fair question, especially when you're trying to get the best rate without ending up with coverage gaps.

A home and auto insurance broker is a licensed professional who works with multiple insurance companies to find coverage that fits your needs. They're your one-stop shop for bundling home and car insurance, comparing options, and making sure you understand what you're buying.

This guide covers understanding your coverage needs, how brokers compare quotes, what to look for when evaluating a broker, and how working with one can help you save. We'll also explain why Morison Insurance might be the trusted partner you're looking for.

A home and auto insurance broker is an independent professional who works with multiple insurance companies, not just one. In Ontario, brokers are licensed and regulated by the Registered Insurance Brokers of Ontario (RIBO), meaning they've met education and ethical standards before advising you on coverage.

Unlike agents who represent a single insurer, brokers work on your behalf. They shop around, compare home and auto policies (including bundling options), and present choices rather than pushing one company's products.

For home and auto insurance specifically, brokers review your unique risks like:

They recommend coverage you might not realize you need (sewer backup, enhanced accident benefits) and help ensure you aren't underinsured or missing key protections.

One often-overlooked benefit? Morison Insurance brokers assist you through the claims process, acting as your advocate when something goes wrong. They explain what's covered, outline next steps, and communicate with the insurer on your behalf if issues arise.

Before getting quotes, have a clear picture of what you need to protect. Knowing your needs helps your broker recommend the right policy and not just the cheapest one.

For home insurance, consider:

For auto insurance, consider:

Don't overlook personal liability coverage on both policies. It protects you if someone is injured on your property or you accidentally cause harm to others.

|

Home Insurance |

Auto Insurance |

Liability |

|

Your dwelling's rebuild cost (not real estate cost) |

Liability limits (consider exceeding the legal minimum) |

Personal liability limits on your home policy |

|

Value of your personal belongings and contents |

Whether you need collision coverage |

Personal liability limits on your auto policy |

|

Common exclusions that may affect you (sewer backup, overland water, earthquakes) |

Whether you need comprehensive coverage |

Whether your limits are adequate if someone is injured on your property |

|

Endorsements you may need for high-value items (jewelry, art, collectibles) |

Deductible amount you can comfortably afford |

Whether you need umbrella coverage for additional protection |

|

Recent updates to your home (roof, electrical, plumbing, heating) |

Your driving record and how it affects rates |

|

|

Safety features (alarm system, smoke detectors, deadbolts) |

Annual kilometres driven and vehicle usage |

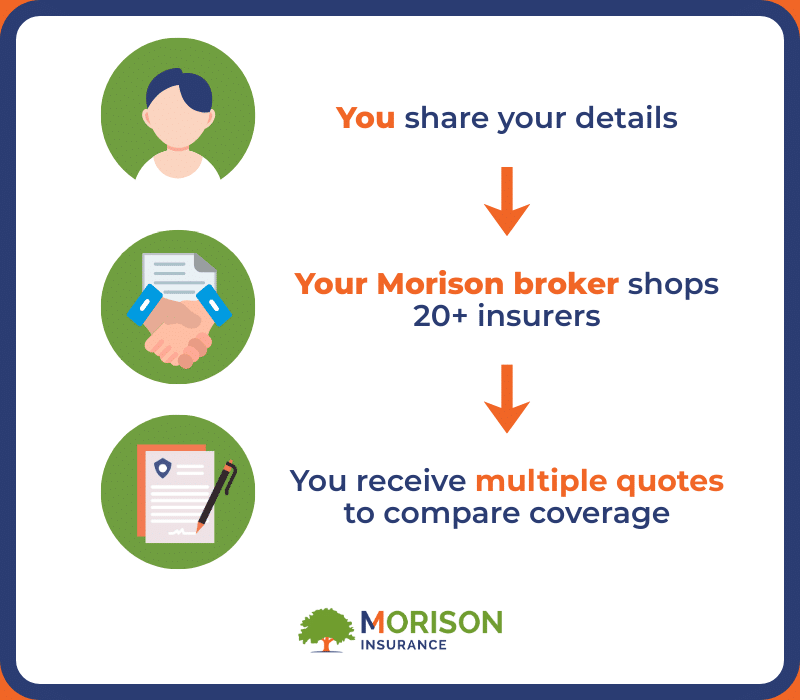

Once you've identified your coverage needs, a broker takes over the legwork:

First, your broker collects your details once; your home information (age, square footage, updates) and vehicle details (make, model, driving record). No filling out multiple forms with different companies.

Next, they shop multiple insurers on your behalf, comparing quotes on an apples-to-apples basis with the same coverage limits, deductibles, and policy options.

Then they present your options, explaining pros and cons in plain language. This is also where bundling discussions happen, as your broker evaluates whether combining policies makes sense for your situation.

|

Get Quotes Yourself |

Use a Broker |

|

|

Time spent |

Hours researching companies, filling out multiple forms, and comparing quotes on your own |

One conversation: your broker handles the shopping and comparison for you |

|

Number of insurers compared |

Limited to companies you know about or find online |

Access to dozens of insurers, including some not available direct-to-consumer |

|

Level of expertise |

You rely on your own knowledge of coverage options and industry terms |

Licensed professionals who understand policy details, exclusions, and endorsements |

|

Risk of missing discounts |

High: you may not know which discounts exist or how to qualify |

Low: brokers know available discounts and ensure you receive everything you're eligible for |

|

Help understanding policy details |

You interpret policy documents on your own |

Your broker explains coverage, exclusions, and fine print in plain language |

|

Support during claims |

You deal directly with the insurance company |

Your broker advocates on your behalf and helps navigate the claims process |

Want help finding the right coverage? Get a quote from Morison Insurance!

Not all brokers are the same. Here's what to look for:

Once your broker presents options, make sure you're comparing like-for-like coverage. Confirm key limits such as home rebuild cost, liability amounts, and vehicle coverage.

Ask your broker to explain what's covered, what's excluded, and which optional endorsements might be worth adding.

Remember: the cheapest quote isn't always the best value when choosing the right insurance policy. A policy with major coverage gaps could cost far more if something goes wrong.

Here's a common misconception: many people assume working with a broker means paying extra. In reality, brokers are typically paid by the insurance companies they work with, not through additional fees charged to you.

You pay the same premium as you would going direct, but you gain expert advice, shopping across multiple insurers, and ongoing support throughout your policy term. Think of it this way: you're already paying for insurance; you might as well get expert help with it.

Yes, and often in ways you might not find on your own. Brokers can apply available discounts you qualify for, such as multi-policy discounts, good driver discounts, winter tire discounts, home alarm discounts, and more.

They can also help you decide whether bundling your home and auto policies makes sense for your situation and suggest deductible options to balance your premium against what you can afford out-of-pocket if you make a claim.

There are many additional ways to save on your car and home insurance. Your broker can walk you through options like usage-based programs, safety features, and home upgrades. For a deeper breakdown, see our guides to car insurance discounts and home insurance discounts.

Bundling means combining your home and auto insurance policies with the same insurer. The typical benefits include fewer bills to manage, aligned renewal dates, and potential savings often up to 25% or more off your premiums.

A broker is well-positioned to evaluate whether bundling is actually the best choice for you. In some cases, keeping policies with separate carriers might offer better coverage or pricing for your specific situation. Your broker can compare both scenarios and recommend the approach that makes the most sense.

A broker is a licensed professional who works with multiple insurance companies to find the right coverage for your needs. They compare quotes, explain options, and support you through claims.

No. Brokers are typically paid by insurance companies, not through extra fees to you. You pay the same or similar premium while gaining expert advice.

This depends on how many insurance partners they work with. A full-service brokerage like Morison Insurance works with dozens of insurers, giving you multiple options.

Yes. Brokers evaluate bundled vs. separate policies to determine which offers the best value for your situation.

Look for RIBO licensing, experience with home and auto coverage, strong reviews, responsive communication, and claims support.

No, you can switch brokers anytime, though it's often easiest at renewal. A good broker earns your loyalty through service, not obligation.

Ready to find the right home and auto coverage for your needs?

Speak with a friendly, RIBO-licensed Morison Insurance broker. We compare quotes from multiple insurers, explain your options in plain language, and help you bundle your home and auto insurance for the right balance of coverage and price.

Call 1-800-463-8074 or request a quote to get started.

This content is written by our Morison Insurance team. All

information posted is merely for educational and informational purposes. It is

not intended as a substitute for professional advice. Should you decide to act

upon any information in this article, you do so at your own risk. While the

information on this website has been verified to the best of our abilities, we

cannot guarantee that there are no mistakes or errors.